TDS for NRI: Why the 2026 Budget Changes Are a Game-Changer for Property Transactions

For years, NRI’s selling property in India suffered enormously due to strict TDS for NRI compliance requirements. Delays in acquiring IT Clearance Certificates and PAN Cards often lead to deals being called off costing NRI’s lakhs of rupees.

The Union Budget 2026 has solved these pain points which were there for ages, in one fell swoop. Reduced to a single page form, made the TAN no longer mandatory and implementation of central declaration form instead of multiple forms, the changes are set to benefit NRI’s selling property in India massively.

What Is TDS for NRI and Why Should You Care About the 2026 Changes?

TDS for NRI represents the tax deducted at source (TDS) applied by a buyer when purchasing immovable property from a Non-Resident Indian.

For NRI transactions, the TDS is applied under Section 195 of the Income Tax Act and without an exemption below a minimum threshold as existed under Section 194-IA for resident-to-resident transactions (applying at above 50 lakhs).

According to an article in Economic Times, the TDS held up deals in 2014-16 cost NRIs lakhs of rupees in delays, typically taking 3-6 more months than resident-to-resident transactions.

Why Were NRIs Losing Lakhs to TDS Delays?

Before 2026, the buyer had to first secure a Tax Deduction Account Number (TAN) to be able to deduct TDS on an NRI seller. It entailed a different application, administration and waiting for over a number of weeks.

During this process, dealing in property was at risk of:

- Deal Fatigue and Buyer Dropouts: Delay in execution compelled the resident buyer to stay back, frustrate and back out of deals and started looking for some properties from resident sellers.

This way a NRI started the concept of selling from scratch, losing time and creating delays for appreciation.

- Losses due to Currencies fluctuation: Since deals were taking 3-6 months to be finalized, for those NRIs who were receiving payments in foreign currency, their equivalent rupee amount got subject to fluctuation in rates.

During bearish market conditions, a delay of 3-6 months might cause a reduction of 5-8% in the finally received rupees.

- Holding Costs Accumulated: In the process of waiting for the TAN approval, the NRI had to spend on the maintenance of the property, municipal taxes and possible Loan Emis.

What Is the Core Change in TDS Rules for NRIs in 2026 Budget?

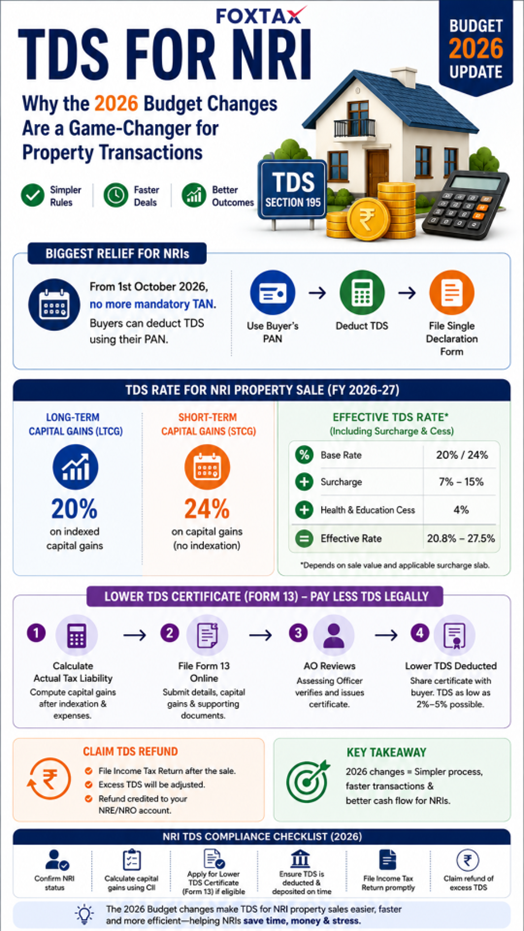

The biggest relief is exempting TDS on property purchase from NRI from mandatory TAN altogether. Since October 1, 2026 property buyers can deduct TDS using its own PAN instead of separate TAN, yet another seemingly insignificant procedural change with huge real-world consequences.

It appears as just one more task for the buyer – calculate TDS on capital gains (or entire sales consideration, if below threshold), deposit it online under its PAN, and file a revised combined TDS declaration form.

What had historically been a several-week exercise in form fill-ups now only takes days, making NRI property transactions as easy as if doing it with another resident.

What Is the New TDS Rate for NRI Property Sale in FY 2026-27?

Knowing the appropriate TDS rate for NRI property sale is important for planning tax efficiently.

For resident tax payers whose property sale consideration exceeds 50 lakh TDS deduction is flat 1% of sale consideration but for NRI TDS deduction is made on capital gain which is sale consideration less purchase consideration.

The base rate is 20% in case of Long-term Capital Gains (LTCG) with indexation and 24% in case of Short-term Capital Gains (STCG) for NRI.

Breaking Down the Effective TDS Rate Including Surcharge and Cess

| Component | Rate | Applicability |

| Base LTCG Rate | 20% | On indexed capital gains |

| Health & Education Cess | 4% | On total tax amount |

| Surcharge | 7%-15% | On exceeding of sale value of more than 50 lakh |

| Effective Rate Range | 20.8% to 27.5% | Covered by value of sale |

For example, when an NRI sells a property with capital gains of.Rs.1 crore, TDS will be Rs. 20 lakh(20% base) + Rs.80,000(4% cess) + surcharge above Rs.50 lakh threshold (amount depends on above mentioned to which slab the NRI lands). Total deducted by the person is around Rs. 22-23 lakhs at before transferring the net sale proceeds. TDS rate for property purchase from NRI also is based on a similar calculation, the person who buys property will deduct the TDS and needs to deposit it.

The 2026 changes do not change the rates though the deduction process is made quite simple.

Can NRIs Obtain a Lower TDS Certificate? (Form 13 Explained)

Yes, NRIs (like ordinary residents) can legally lower the TDS burden through a Lower Deduction Certificate ( Section 197 of Income Tax Act ). This certificate permits NRI buyers to deduct TDS at a much lower rate based on NRI’s actual liability.

Step-by-Step Process for Getting a Lower TDS Certificate for NRI

The process for applying needs to be filed before sale transaction of property with the Jurisdictional AO:

- Calculate Actual Tax Liability: Calculate your net capital gains using indexation benefits and costs of acquisition and improvements to arrive at your actual capital gains. Use this value to request for a lower rate.

- File Form 13 Online: Look for Income Tax e-file portal. Submit Form 13 covering details of property, estimated capital gains and the reduced rate of TDS claimed. Supporting documentation to be submitted is Sale Deed, Purchase Deed and calculation of consumer price index.

- AO Review and Certificate Issuance: Usually 15-30 days by the Assessing Officer.

- Once approved, a certificate stating the rate of TDS (sometimes as low as 2-5% of sale value) is issued. Share this certificate with the buyer before the TDS deduction date.

After the lower TDS certificate for NRI is received for NRI, the NRI buyer pays the lower TDS on the purchase. Thereafter, the NRI buyer has to file his annual income tax return to pay the balance TDS or claim the refund if additional TDS was deducted.

Foxtax can help NRI to get the lower TDS certificate in the most efficient way.

How Foxtax Simplifies NRI TDS Compliance for Property Transactions

The challenge for a NRI in rules for TDS for NRI when selling property in India involve crossborder tax rules, capital gains calculations and rules for Indian income tax. Foxtax specializes in the rules with good knowledge of Indian income tax rules, Indian capital gains rules and crossborder tax to sell property in India.

From right TDS numbers for TDS rate for NRI property sale to prepare indexation benefit calculations to minimize capital gains of sale, all the tax planning required for the sale of property is done by Foxtax for its clients.

Quick Glance: Your 2026 NRI TDS Compliance Checklist

Before sale of property in India as NRI, under the new 2026 rules, carry out these:

- Verify that you are treated as NRI (by satisfying Residential Status as per Income Tax Act) so that Section 195 ( if TDS for NRI ) or Section 194-IA ( an NRI transaction ) applies.

- Calculate it via Cost Inflation Index (CII) tables to get actual amount of capital gain tax payable, without deducting any TDS.

- If the actual tax payable is much below the TDS rate, apply for a Lower Deduction Certificate (Form 13) which will result in crores unblocked tax.

- Inform the buyer of the new PAN based TDS procedure from October 2026 so he doesn’t apply for a TAN or follows the incorrect rules.

- File your income tax return immediately after the sale to get an immediate refund of any excess TDS. Specify the correct NRE/NRO account number for quick credit.

Infographic explaining TDS for NRI property sale including Section 195 rates, surcharge, lower TDS certificate process, and refund rules for 2026

Conclusion

The 2026 Budget changes mark the biggest TDS simplification for NRI property sales since the 2004 introduction of TDS.

Removal of the mandatory TAN requirement and introduction of a new PAN based TDS deduction method are all tremendous wins for NRIs, saving lakhs per delayed deal and lost deal opportunity.

If you plan to sell residential property, commercial real estate or land soon, consider understanding the new TDS rate for NRI property sale and the lower TDS certificate process for maximum sale proceeds.

Frequently Asked Questions About TDS for NRI

Q1: What is the threshold limit for TDS on NRI property sales?

Unlike resident transactions under 194-IA (limit 50 lakh), TDS on payment to NRI for purchase of immovable property under 195 is on FULL sale value (not limit). Even if you sell property of 30 lakh, TDS must be deducted.

Q2: Can an NRI claim a TDS refund if excess tax was deducted?

Definitely yes.

In case the TDS(20% + surcharge & cess) deducted by the buyer on the purchase price was at higher rate than the actual Capital Gain Tax payable after indexation, then the excess amount can be claimed as refund at the time of filing IT return by providing the correct Indian Bank details for direct credit.

Q3: What happens if the buyer does not deduct TDS from an NRI seller?

The buyer would be penalized severely – disallowing property expense in the return, interest on late deduction, and even prosecution. The Income Tax Department can recover the tax from the seller with interest for the NRI.

Always complete the TDS formalities before transferring sale proceeds.

Q4: Are the 2026 TDS changes applicable to all property types?

YES, the reduced PAN based TDS deduction will be applicable to all immovable property transactions by NRI sellers, be it residential apartment, independent house, Commercial space or land parcel(s). The date of effect being 01 October 2026 will be the same for all categories of properties.