Navigating Goods and Services Tax (GST) compliance requires timely return filing. Missing deadlines incurs penalties and interest. Understanding these charges is crucial for every registered person. This guide clarifies GST late fees and interest, helping businesses avoid unnecessary costs.

What Are GST Late Fees?

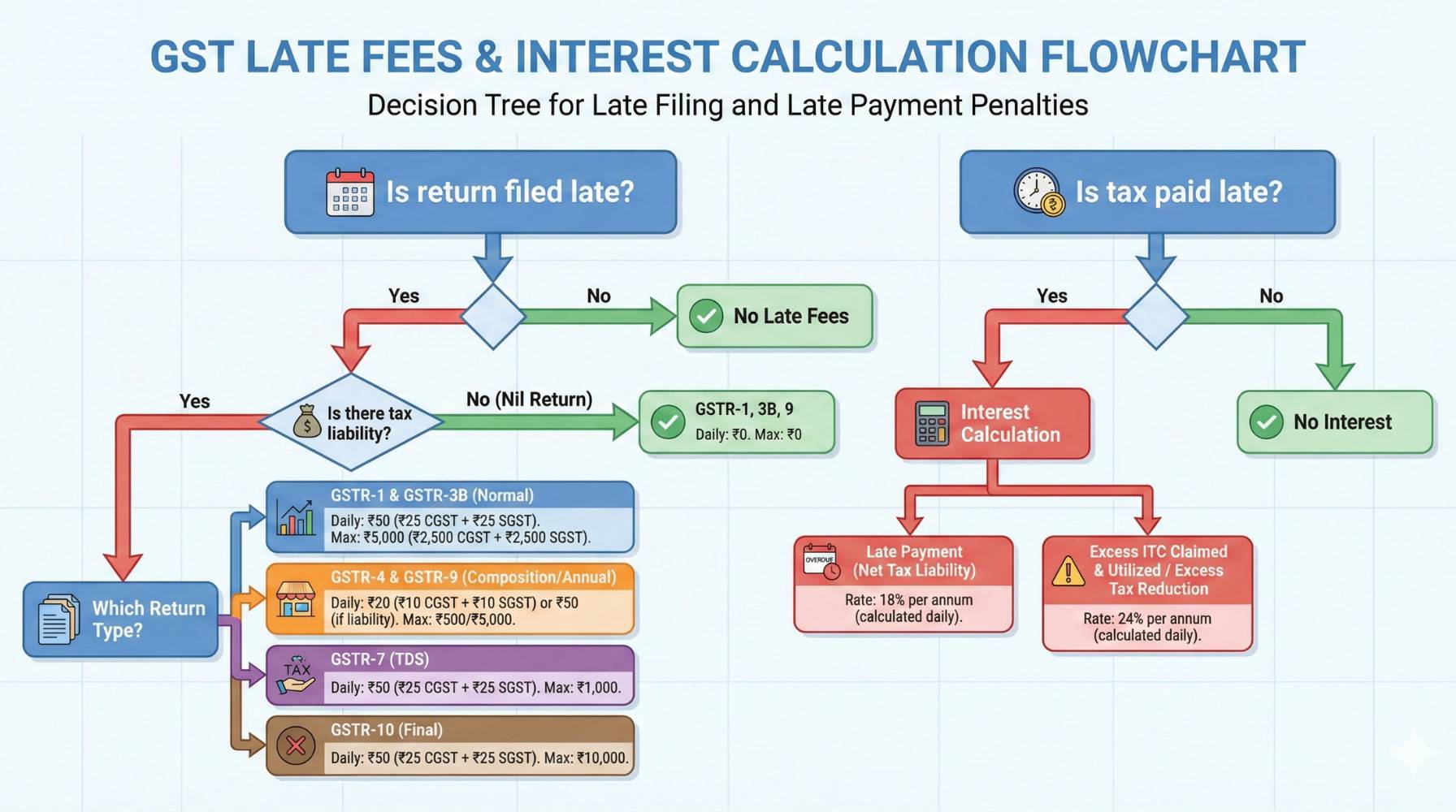

GST late fees are statutory penalties levied for delayed filing of GST returns. Every registered person must submit their GST returns by the specified due date. Failure to do so attracts a daily fee. The legal framework for these penalties is robust.

The Legal Basis Under the CGST Act

The foundation for GST late fees is established under Section 47 of the Central Goods and Services Tax (CGST) Act 2017. This section empowers the government to impose late fees on taxpayers who fail to file their returns (such as Form GSTR-1, Form GSTR-3B, Form GSTR-4, Form GSTR-7, and Form GSTR-10) within the prescribed timeframe. The Central Board of Indirect Taxes and Customs (CBIC) issues notifications to specify exact fee amounts and any changes.

GST Late Fee Calculation for Every Return Type

The calculation of GST late fees varies based on the type of return and the taxpayer’s turnover. Understanding these specific rules is vital for compliance. This section details the GST late fee penalty for filing GSTR-3B after due date and other returns.

For Monthly/Quarterly Returns (GSTR-1 & GSTR-3B)

For regular taxpayers filing Form GSTR-1 (supply details) and Form GSTR-3B (summary return), late fees depend on the presence of a tax liability.

- Nil returns: If you have no outward supplies, inward supplies, or tax liability for the period (a nil return), the late fee is ₹20 per day (₹10 CGST + ₹10 SGST). The minimum GST late fee for nil return filing is therefore ₹20 per day. The maximum cap for nil returns is ₹500 (₹250 CGST + ₹250 SGST).

- Returns with tax liability: If there is any tax liability, the late fee increases to ₹50 per day (₹25 CGST + ₹25 SGST). This is relevant for how to calculate GST late fees for small businesses with turnovers up to ₹5 Cr. The maximum cap for returns with tax liability is ₹10,000 (₹5,000 CGST + ₹5,000 SGST). This addresses the late fee for GSTR-1 filing after due date calculation.

For Annual Returns (GSTR-9)

The Annual Return filed in Form GSTR-9 also carries a late fee for delayed submission. The late fee for Form GSTR-9 is 0.25% of turnover (0.25% CGST + 0.25% SGST) in the state or union territory. There is no specific maximum cap, as it’s a percentage of Annual Aggregate Turnover (AATO). For FY 2022-23, CBIC Notification No. 07/2023–Central Tax provided a reduced late fee. For taxpayers with an AATO exceeding ₹5 crore, the maximum late fee was capped at ₹20,000 (₹10,000 CGST + ₹10,000 SGST). This affects the GST late fee for annual return GSTR-9 filing delay.

For Composition Scheme Returns (GSTR-4)

Taxpayers under the Composition Scheme file Form GSTR-4.

- For a nil return, the late fee is ₹20 per day (₹10 CGST + ₹10 SGST), capped at ₹500 (₹250 CGST + ₹250 SGST).

- For returns with tax liability, the late fee is ₹50 per day (₹25 CGST + ₹25 SGST), capped at ₹5,000 (₹2,500 CGST + ₹2,500 SGST). This addresses the GST late fee for composition dealers delayed filing.

For TDS Returns (GSTR-7)

Entities required to deduct Tax Deducted at Source (TDS) under GST file Form GSTR-7. The late fee for Form GSTR-7 is ₹50 per day (₹25 CGST + ₹25 SGST). The maximum cap for Form GSTR-7 is ₹2,000 (₹1,000 CGST + ₹1,000 SGST).

For Final Returns (GSTR-10)

Upon cancellation of GST registration, a Final Return must be filed in Form GSTR-10. The late fee for Form GSTR-10 is ₹50 per day (₹25 CGST + ₹25 SGST). This fee is levied as per Section 47 of the CGST Act and continues daily until the return is filed, with no specific maximum cap mentioned in the law.

Here’s a summary of the GST late fees:

| Return Type | Scenario | Late Fee (per day) | Maximum Cap (CGST + SGST) |

| GSTR-1 & GSTR-3B | Nil Return | ₹20 (₹10 CGST + ₹10 SGST) | ₹500 (₹250 CGST + ₹250 SGST) |

| Tax Liability | ₹50 (₹25 CGST + ₹25 SGST) | ₹10,000 (₹5,000 CGST + ₹5,000 SGST) | |

| GSTR-9 | Turnover > ₹5 Cr | 0.25% of turnover | No Cap (Max 0.25% of AATO) |

| FY 2022-23 (Reduced) | 0.04% of turnover | ₹20,000 (₹10,000 CGST + ₹10,000 SGST) | |

| GSTR-4 | Nil Return | ₹20 (₹10 CGST + ₹10 SGST) | ₹500 (₹250 CGST + ₹250 SGST) |

| Tax Liability | ₹50 (₹25 CGST + ₹25 SGST) | ₹5,000 (₹2,500 CGST + ₹2,500 SGST) | |

| GSTR-7 | All Scenarios | ₹50 (₹25 CGST + ₹25 SGST) | ₹2,000 (₹1,000 CGST + ₹1,000 SGST) |

| GSTR-10 | All Scenarios | ₹50 (₹25 CGST + ₹25 SGST) | No Cap (Daily until filed) |

Understanding Interest on Late Payment of GST

In addition to late fees for delayed filing, interest is charged on delayed tax payments. This is a separate charge.

What is the interest rate for delayed GST payments?

Interest is charged at a rate of 18% per annum on the unpaid GST amount from the due date until the actual date of payment. This applies to any delayed payment of tax. A higher interest rate of 24% per annum is applicable for the undue or excess claim of input tax credit or excessive reduction in output tax liability. This higher rate is a critical consideration for businesses. A GST late fee interest calculator online can assist in estimating these charges.

How is interest different from a late fee?

It is crucial to distinguish between a late fee and interest.

- A late fee is levied for delayed filing of GST returns, regardless of whether tax was due or paid. It is a penalty for procedural non-compliance.

- Interest is charged specifically for delayed tax payment. It compensates the government for the time value of money. For example, if you pay your tax on time but file Form GSTR-3B late, you will incur a late fee but no interest. If you pay your tax late, you will incur both late fees (if the return is also late) and interest. Input Tax Credit (ITC) cannot be used to discharge late fees.

How to Pay GST Late Fees and Interest

Payment of GST late fees and interest follows specific procedures on the GST portal.

Can I use Input Tax Credit (ITC) to pay late fees?

No. Input Tax Credit (ITC) cannot be utilized to pay GST late fees or interest. These charges must be settled through a cash payment. Taxpayers need to deposit funds into their electronic cash ledger via net banking, credit/debit card, or NEFT/RTGS, and then use this balance to pay the late fees and interest. This explains how to pay GST late fees through GST portal.

Is the late fee calculation automatic?

Yes, the GST system automatically calculates the late fee when you attempt to file a delayed return. The system determines the number of days of delay from the due date and applies the relevant daily late fee. This automated calculation helps ensure accuracy.

Can GST Late Fees Be Waived or Reduced?

While late fees are statutory, the government sometimes provides relief through waivers or reductions.

The Government’s Power to Grant Waivers

Section 128 of the CGST Act empowers the government to waive or reduce late fees through official notifications. This discretionary power allows the CBIC to provide relief to taxpayers under specific circumstances, often during economic downturns or for compliance drives. Such waivers are typically granted for specific return types or financial years.

Recent Examples of GST Late Fee Waivers

The government has historically offered waivers to ease compliance burdens. For example, CBIC Notification No. 08/2025 – Central Tax provided specific relief. It waived late fees for filing Form GSTR-9C (reconciliation statement) for financial years 2017-18 to 2022-23, provided the returns were filed by March 31, 2025. Such notifications provide late fee exemption for first time GST return defaulters or those under specific conditions. While no specific late fee waiver for GST return filing 2026 has been announced yet, it is common for the government to issue such relief periodically for various compliance challenges.

Frequently Asked Questions

1. Can I file Form GSTR-3B without paying the late fee?

No. The GST system will not allow you to file Form GSTR-3B if there is a pending late fee. You must pay the calculated late fee first.

2. Is there a late fee for filing a nil Form GSTR-1?

Yes. Even for a nil return in Form GSTR-1, a late fee of ₹20 per day (₹10 CGST + ₹10 SGST) is applicable, capped at ₹500 (₹250 CGST + ₹250 SGST).

3. How can I check my pending GST late fees?

You can check your pending GST late fees directly on the GST portal when you attempt to file a delayed return. The system automatically calculates and displays the exact amount due based on the delay from the due date.

topic: GST Late Fees Schema: